Surprisingly, understanding your billing cycle takes less than 10 minutes. Moreover, once you grasp how it works, you can time your purchases to get up to 50 interest-free days on every transaction — legally, consistently, and without any tricks.

Most credit card users in India focus on rewards and cashback — but they completely ignore the one thing that can either save them thousands of rupees or cost them dearly every single month. 💡 That thing is the billing cycle.

In this guide, we break down exactly how credit card billing cycles work in India, what the RBI mandates about your statement, and how to use your billing cycle smartly to protect both your wallet and your CIBIL score.

Table of Contents

- What Is a Credit Card Billing Cycle?

- How the Billing Cycle Works — Step by Step

- Statement Date vs Due Date — Key Differences

- The Grace Period — Your Interest-Free Window

- How to Get Up to 50 Interest-Free Days

- How the Billing Cycle Affects Your CIBIL Score

- What RBI Rules Say About Your Billing Statement

- How to Change Your Billing Cycle Date in India

- Common Billing Cycle Mistakes to Avoid

- Final Verdict

1. What Is a Credit Card Billing Cycle?

A credit card billing cycle refers to the fixed monthly period during which your bank tracks every rupee you spend on your card. In India, most banks run billing cycles that last between 25 and 31 days. At the end of this period, the bank generates your monthly statement showing your total outstanding balance, minimum amount due, due date, and a full transaction breakdown.

In simple terms, think of the billing cycle as a monthly window that opens and closes on fixed dates. Whatever you spend inside that window appears on one statement. Whatever you spend after it closes rolls into the next cycle.

“Your billing cycle is the financial heartbeat of your credit card. Master it, and you master your money.” — Simplix Finance Desk

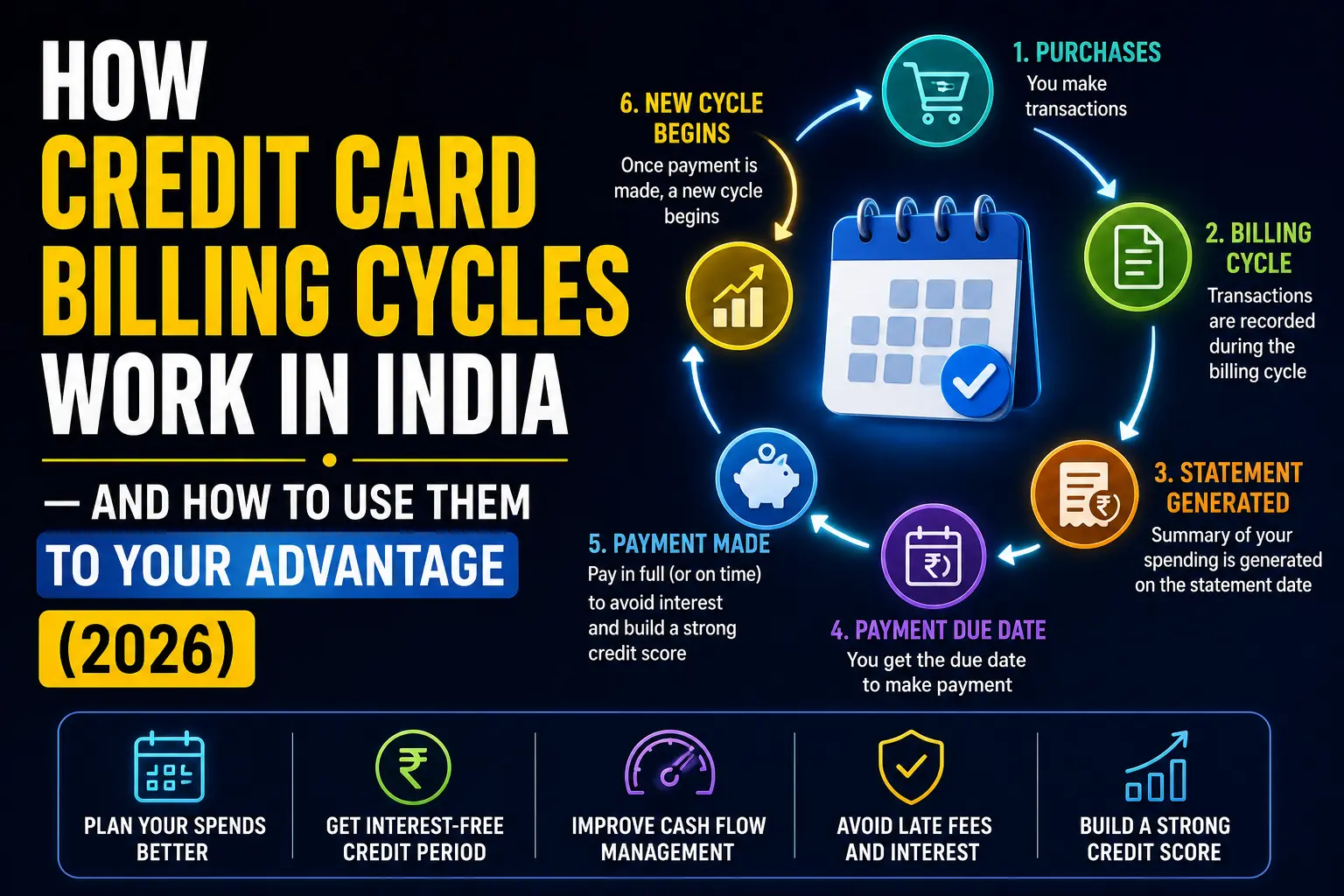

2. How the Billing Cycle Works — Step by Step

To understand this clearly, let us walk through a real example. Suppose your billing cycle runs from the 11th of one month to the 10th of the next month — and your bank generates your statement on the 10th.

Step 1 — Your Cycle Opens

On the 11th, your new billing cycle begins. From this date, your bank starts tracking every transaction you make on your card.

Step 2 — You Spend During the Cycle

Throughout the month, you use your card for groceries, online shopping, fuel, dining — whatever your regular expenses look like. The bank records every transaction in real time.

Step 3 — The Bank Generates Your Statement

On the 10th of the following month, your cycle closes and the bank generates your statement. This statement shows your total outstanding balance, a breakdown of every transaction, the minimum amount due, and your payment due date.

Step 4 — Your Grace Period Begins

After the bank generates your statement, your grace period starts. Most Indian banks give you 18 to 21 days from the statement date to repay. Therefore, if your statement date falls on the 10th, your due date typically lands around the 28th to 31st of that same month.

Step 5 — You Repay and the Cycle Resets

If you pay the full outstanding amount before the due date, the bank charges you zero interest. As a result, your available credit limit resets and a fresh cycle begins on the 11th again.

3. Statement Date vs Due Date — Key Differences

Many cardholders confuse these two dates — and that confusion leads to missed payments and unnecessary interest charges. Furthermore, mixing them up can directly damage your CIBIL score. Here is the clear difference:

| Term | What It Means | Example |

|---|---|---|

| Statement Date | The date your bank closes the cycle and generates your bill | 10th of every month |

| Due Date | The last date to repay without incurring interest | 28th–31st of the same month |

| Grace Period | The interest-free window between statement date and due date | 18–21 days typically |

| Billing Cycle Start | The day after your statement date — your new cycle begins | 11th of every month |

Importantly, the due date is not the same as the statement date. Many first-time cardholders pay on the statement date thinking it is already late — when in reality, they still have 18 to 21 days left in their grace period.

4. The Grace Period — Your Interest-Free Window

The grace period refers to the interest-free window your bank gives you between your statement date and your due date. During this window, your outstanding balance carries zero interest — as long as you pay the full amount before the due date.

According to RBI guidelines, banks must give cardholders at least 14 days to pay their bill before charging any interest. However, most major Indian banks — HDFC, SBI, ICICI, and Axis — offer 18 to 21 days as standard practice, which gives you more breathing room than the minimum mandate.

Consequently, if you always pay your full outstanding balance within the grace period, you essentially borrow money from the bank for free every single month. That is the real power of understanding your billing cycle.

The RBI mandates that banks must show you exactly how long it would take to clear your balance if you paid only the minimum due every month. Check that number on your next statement — it is usually eye-opening enough to motivate full payment. — Simplix Finance Desk

5. How to Get Up to 50 Interest-Free Days

This is where billing cycle knowledge becomes genuinely powerful. With the right timing, you can stretch your interest-free window to nearly 50 days on a single purchase — without doing anything unusual.

Here Is How It Works

Suppose your billing cycle runs from the 11th to the 10th and your due date falls on the 30th. If you make a purchase on the 11th — the very first day of your new cycle — that transaction will not appear on your statement until the 10th of next month. You then get the full grace period on top of that.

In total, that gives you approximately 49 to 50 days of interest-free credit on that purchase — the remaining days of the current cycle plus the full grace period.

On the other hand, if you make the same purchase on the 9th — one day before your cycle closes — that transaction appears on the very next statement. Consequently, you only get the 18 to 21 day grace period, not the full 50 days.

Practical Rule to Remember

Make large purchases — electronics, appliances, travel bookings — on or just after your statement date. This maximises the interest-free window and gives you the most time to repay without any cost.

| Purchase Timing | Interest-Free Days Available |

|---|---|

| Day 1 of new cycle (11th) | ~49–50 days ✅ Maximum |

| Middle of cycle (25th) | ~34–35 days |

| Last day of cycle (10th) | ~18–21 days ⚠️ Minimum |

6. How the Billing Cycle Affects Your CIBIL Score

Your billing cycle directly connects to your CIBIL score in two important ways that most cardholders never realise.

Payment Timing — The Biggest Factor

Your bank reports your payment behaviour to credit bureaus every month. If you miss your due date — even by one day — the bank flags it as a late payment. Furthermore, from 2026, banks report this data every 15 days under the new RBI mandate, meaning a missed payment hits your CIBIL score significantly faster than before.

Credit Utilisation — The Hidden Factor

Your bank also reports your outstanding balance at the time of reporting — which may not always fall on your statement date. Therefore, even if you pay your bill in full every month, carrying a high balance mid-cycle can temporarily push your credit utilisation above 30% and hurt your score. To avoid this, try to keep your spending below 30% of your credit limit throughout the month — not just at the time of payment.

7. What RBI Rules Say About Your Billing Statement

The RBI introduced significant billing transparency rules in 2025–26 that directly benefit Indian cardholders. Here is what your bank must now legally provide on every statement:

- Transaction date and posting date — separately listed for every purchase

- Merchant name and location — clearly mentioned for every transaction

- Exact amount in Indian rupees — with all applicable charges broken out separately

- A detailed fee breakup — annual fees, late payment charges, interest charges — all itemised

- Minimum payment repayment timeline — how long it will take to clear your balance paying only the minimum due

Additionally, the RBI prohibits banks from adding delayed entries to your statement without clear disclosure. In other words, your bank cannot sneak in a charge days after your cycle closes without explicitly notifying you. If your bank violates any of these rules, you have the right to raise a formal complaint through the RBI’s Banking Ombudsman.

8. How to Change Your Billing Cycle Date in India

Many Indians struggle because their credit card due date does not align with their salary date. Fortunately, the RBI addressed this directly. Since March 2024, the RBI gives every cardholder the right to change their billing cycle date at least once as per their personal financial schedule.

For example, if your employer credits your salary on the 1st of every month, you can request a due date around the 5th to 10th. This way, your salary arrives before your credit card bill comes due — making repayment far more manageable.

How to Request a Billing Cycle Change

- HDFC Bank — Call customer care or request via net banking

- SBI Card — Call 1860 180 1290 or visit the SBI Card app

- ICICI Bank — Request via iMobile Pay app or customer care

- Axis Bank — Request via Axis Mobile app or customer care

Moreover, most banks process this change within one to two billing cycles. Plan ahead and make the request at least 30 days before you need the new date to take effect.

9. Common Billing Cycle Mistakes to Avoid

Even experienced cardholders make these mistakes. Therefore, go through this list and check whether any apply to you right now.

- Confusing the statement date with the due date — paying on the statement date when you still have 18–21 days left, or worse, missing the due date thinking it is the statement date

- Paying only the minimum due — the remaining balance immediately attracts interest at 24%–48% per year. Furthermore, this behaviour shows up negatively on your CIBIL report

- Making large purchases right before the cycle closes — you lose most of your interest-free window. Instead, time big purchases for the start of a new cycle

- Not setting up autopay — missing a due date because you forgot is entirely avoidable. Set autopay for the full outstanding amount the day you receive your card

- Ignoring mid-cycle utilisation — your bank may report your balance mid-cycle, not just on the statement date. Therefore, keeping your spending consistently below 30% of your limit matters throughout the month

- Not reading your statement — under the new 2025–26 RBI rules, banks must itemise every charge. Consequently, reviewing your statement each month helps you spot errors, hidden fees, or unauthorised transactions immediately

10. Final Verdict

Your credit card billing cycle is not just administrative fine print — it is a financial tool that works either for you or against you, depending on how well you understand it. Fortunately, the mechanics are straightforward once you see them clearly.

Know your statement date. Know your due date. Time large purchases to maximise interest-free days. Set up autopay so you never miss a payment. And check your statement every month — not just the total due, but every line item.

Do all of this consistently, and your billing cycle becomes one of the most powerful free financial tools in your wallet. Moreover, it directly protects and builds your CIBIL score at the same time.

The rule is simple: your billing cycle rewards the organised and punishes the forgetful. Decide which one you want to be.

Read Next on Simplix

- What Is a Credit Card? A Complete Beginner’s Guide for India

- What Is a CIBIL Score? How It Works and Why It Matters

- The Minimum Due Trap — Why Paying Less Is Costing You More

Want to pick a credit card with a billing cycle that works for your salary date?

Simplix has curated the best credit cards in India — compared by grace period, rewards, and eligibility so you find the right fit without the confusion.

👉 Explore Best Lifetime Free Credit Cards in India

Never miss a payment again — Follow Simplix on Instagram for weekly finance tips, card alerts, and smarter money decisions.

👉 Follow Simplix on Instagram → Simplix MultiVentures