Imagine applying for a home loan after years of saving — only to get rejected because of a three-digit number you never knew existed. 😳 In fact, that is the reality for millions of Indians every year.

Your CIBIL score is one of the most important numbers in your financial life. In fact, it decides whether a bank approves your loan, what interest rate you get, and even whether your credit card application goes through. Yet most people only discover it the day a bank turns them down.

In this guide, we break down exactly what a CIBIL score is, how CIBIL calculates it, what damages it, what the new 2026 RBI rules mean for you — and most importantly, how to build and protect your credit health over time.

Table of Contents

- What Is a CIBIL Score?

- What Is CIBIL — and Who Calculates Your Score?

- The CIBIL Score Range — What Each Number Means

- How Is Your CIBIL Score Calculated?

- What Is Credit Health — and How Is It Different?

- What Hurts Your CIBIL Score

- How the New 2026 RBI Rules Change Everything

- How to Check Your CIBIL Score for Free

- How to Improve Your CIBIL Score

- Final Verdict

1. What Is a CIBIL Score?

A CIBIL score is a three-digit number between 300 and 900 that represents your creditworthiness — how likely you are to repay a loan or credit card bill on time, based on your past financial behaviour.

The higher your score, the more trustworthy you appear to lenders. Lenders consider a score of 750 and above as good in India. According to TransUnion CIBIL’s own data, approximately 79% of all loans sanctioned in India go to borrowers with a score of 750 or above. As a result, if your score is below that, you either get rejected or end up paying significantly higher interest rates.

In simple terms, Think of it as your financial report card — except banks check it before they decide to lend you money, not after.

“Your CIBIL score is being calculated every month whether you know about it or not. Banks check it before they call you back, before they approve your card, before they decide your interest rate.” — Simplix Finance Desk

2. What Is CIBIL — and Who Calculates Your Score?

CIBIL stands for Credit Information Bureau (India) Limited — India’s oldest and most widely used credit bureau, established in 2000. Over time, the word “CIBIL score” has become the generic term for credit score in India — the way “Google” became a verb for searching.

However, CIBIL is not the only bureau. The RBI has licensed four credit bureaus in India; each bureau calculates your score independently:

| Credit Bureau | Score Name | Most Used By |

|---|---|---|

| TransUnion CIBIL | CIBIL Score | Most Indian banks — HDFC, SBI, Axis, ICICI |

| Experian India | Experian Credit Score | NBFCs and digital lenders |

| CRIF High Mark | CRIF Score | Microfinance institutions, NBFCs |

| Equifax India | Equifax Score | Some banks and fintech lenders |

All four use the same 300–900 range and the same underlying lender data. That said, scores differ slightly across bureaus but will be broadly in the same range. For most purposes, monitor your TransUnion CIBIL score as your primary benchmark — it is what the majority of Indian banks check first.

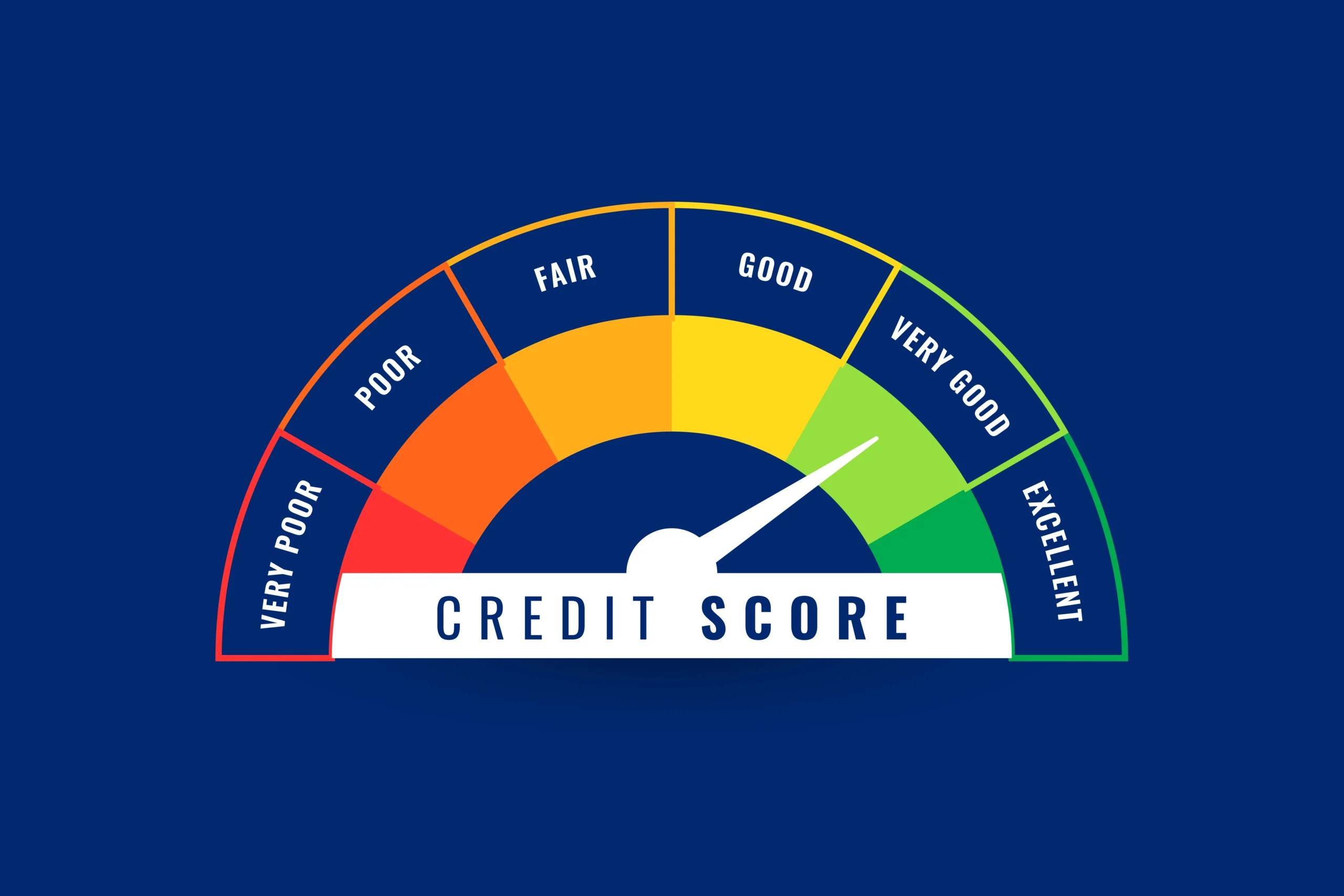

3. The CIBIL Score Range — What Each Number Means

Here is exactly how lenders in India read your score:

| Score Range | Rating | What It Means for You |

|---|---|---|

| 750 – 900 | Excellent ✅ | Best loan terms, lowest interest rates, fast approvals |

| 700 – 749 | Good 👍 | Likely approved, slightly higher interest rates |

| 650 – 699 | Fair ⚠️ | May be approved with stricter terms or a co-applicant |

| 550 – 649 | Poor ❌ | Most banks will reject — NBFCs may approve at high rates |

| 300 – 549 | Very Poor ❌ | Very likely rejected across all lenders |

| -1 / NH | No History | No credit file yet — not bad, but invisible to lenders |

Moreover, the gap between 680 and 750 is more costly than most people realise. On a ₹10 lakh personal loan over 5 years, that difference alone can cost you ₹1–2 lakh in extra interest paid over the loan tenure. A good score is not just about approval — it is about the price you pay for money.

4. How Is Your CIBIL Score Calculated?

Your CIBIL score is not random. CIBIL calculates your score using five specific factors, each weighted differently. Therefore, understanding these weights is the key to improving your score deliberately.

| Factor | Weight | What It Tracks |

|---|---|---|

| Payment History | 35% | Whether you pay EMIs and credit card bills on time |

| Credit Utilisation | 30% | How much of your credit limit you are using |

| Credit Age | 15% | How long you have been using credit products |

| Credit Mix | 10% | Balance of secured loans (home, car) and unsecured credit (cards, personal loans) |

| New Enquiries | 10% | How many times lenders have pulled your credit report recently |

Payment History — The Single Biggest Factor

At 35% of your total score, this is the most important factor by far. Every missed EMI, delayed credit card payment, or loan default leaves a mark. One missed payment can drop your score by 50–100 points depending on your current score. Conversely, consistently paying on time every month is the single most powerful thing you can do for your credit health.

Credit Utilisation — The Often Ignored Factor

This is the percentage of your total available credit limit that you are currently using. If your credit card limit is ₹1,00,000 and your outstanding balance is ₹70,000, your utilisation is 70% — which is too high. Keep your credit utilisation below 30% at all times. High utilisation signals financial stress to lenders, even if you are paying on time.

Credit Age — Why Old Accounts Matter

The longer your credit history, the better. This is why closing your oldest credit card is almost always a bad idea — it reduces the average age of your credit accounts and can hurt your score. Building your first CIBIL score from scratch takes approximately 6 months of active credit product usage.

5. What Is Credit Health — and How Is It Different?

Your CIBIL score tells lenders how you have repaid debt in the past. Your credit health is a broader picture — it reflects the overall state of your credit profile, not just one number.

In 2026, the RBI introduced a supplementary metric called the Credit Health Score (CHS). Unlike your CIBIL score, the CHS factors in:

- Income stability signals

- The frequency of hard enquiries in the last 6 months

- The diversity of your credit types — secured versus unsecured

Lenders primarily use the CHS during the loan underwriting process, and it directly influences both approval rates and the interest rate they offer you. Your CIBIL score remains the primary benchmark — you still need 750+ for the best loan offers. The CHS is an additional lens lenders now use alongside it.

Think of your CIBIL score as your exam result and your credit health as your overall academic record — attendance, behaviour, consistency, and all. Lenders now look at both. — Simplix Finance Desk

Maintaining good credit health means paying on time, keeping utilisation low, not applying for multiple credit products at once, and having a healthy mix of credit types — all habits that also improve your CIBIL score naturally.

6. What Hurts Your CIBIL Score

Most damage to credit scores happens from habits people do not even realise are harmful. Here is what to actively avoid:

- Missing EMI or credit card payments — even by one day. This is the fastest way to damage your score.

- Paying only the minimum due on your credit card. The remaining balance starts attracting interest and signals incomplete repayment behaviour to bureaus.

- Using more than 30% of your credit limit consistently — even if you pay in full every month.

- Applying for multiple loans or credit cards in a short period — each application triggers a hard enquiry that temporarily lowers your score.

- Closing your oldest credit card — it reduces your credit history length and available credit limit simultaneously.

- Loan settlements — settling a loan for less than the full amount is recorded as “Settled” on your report, not “Closed.” It stays on your file for years and is viewed very negatively by lenders.

- Being a guarantor for someone who defaults — their missed payments directly impact your score too.

7. How the New 2026 RBI Rules Change Everything

The RBI has introduced significant reforms to India’s credit reporting system in 2025–26. These changes directly affect how fast your score moves — in both directions.

Fortnightly Reporting — Your Score Updates Faster

Previously, lenders reported your credit data to bureaus once a month. From 2026, the RBI has mandated that all scheduled commercial banks and major NBFCs report credit data every 15 days — with some moving towards weekly updates. This means your score now reflects your financial behaviour almost in real time.

The impact is significant in both directions. If you make a payment today, it could reflect on your report within days — not weeks. But equally, a missed EMI or a sudden spike in credit utilisation will also show up much faster than before.

Faster Dispute Resolution

Previously, resolving a wrong entry on your credit report could take 45–60 days with no guaranteed outcome. Under the new RBI directive, lenders and bureaus must resolve all disputes within 30 calendar days. If not resolved within 30 days, the disputed information must be temporarily removed from your report until resolution.

Free Credit Report Every Quarter

Earlier, you were entitled to one free credit report per year. The RBI now mandates that every Indian is entitled to one free credit report every quarter — four times a year. Use this. Checking your own report does not affect your score — it is a soft enquiry.

Derogatory Marks Removed After 7 Years

Any negative marks — settled accounts, written-off loans, late payments — must now be removed from your credit file after 7 years, consistent with international best practices. This gives people a genuine opportunity to rebuild their credit health after a difficult financial period.

8. How to Check Your CIBIL Score for Free

You can check your CIBIL score through the following official and trusted channels:

- TransUnion CIBIL official website — cibil.com — one free report every quarter as mandated by RBI

- Your bank’s mobile app — most major banks (HDFC, SBI, Axis, ICICI) now show your CIBIL score inside the app for free

- RBI-authorised fintech platforms — several licensed platforms offer free score checks with no impact on your score

Always check your score on the official CIBIL website or your bank’s app first before using third-party platforms. And remember — checking your own score is a soft enquiry and has zero impact on your score. Only lender-initiated checks (hard enquiries) affect it.

9. How to Improve Your CIBIL Score

Improving your CIBIL score is not complicated — but it does require consistency over time. There are no shortcuts. Here is what actually works:

Pay Every Bill on Time — Without Exception

Set up autopay for all your loan EMIs and credit card bills immediately. Even one missed payment can drop your score significantly. With the new 2026 fortnightly reporting rules, that missed payment will show up on your report within days — not weeks.

Keep Credit Utilisation Below 30%

If your combined credit limit across all cards is ₹2,00,000, make sure your total outstanding balance stays below ₹60,000 at all times — not just at the time of payment. Banks report your balance at various points in the billing cycle.

Do Not Apply for Multiple Credit Products at Once

Every loan or card application triggers a hard enquiry. Multiple hard enquiries in a short period signal financial desperation to lenders and drop your score. Space out applications by at least 3–6 months.

Keep Old Accounts Open

Even if you do not use an old credit card regularly, keep it open. The credit history length and available limit it contributes to your profile are valuable. Make one small purchase on it every few months to keep it active.

Build a Healthy Credit Mix

Having both secured loans (home loan, car loan) and unsecured credit (credit cards, personal loans) signals a balanced borrower. You do not need to take loans just for this — but if you do have a mix naturally, manage all of them well.

If You Have No Score — Start With a Secured Credit Card

A score of -1 or NH (No History) means lenders have no data on you. The fastest way to build a score from scratch is to get a secured credit card — issued against a fixed deposit — use it for small purchases, and pay the full amount every month. Within 6 months, you will have a trackable score.

10. Final Verdict

Your CIBIL score is not just a number — it is the financial reputation you build every single month through your repayment habits. It determines whether you get a home loan, a car loan, or a credit card — and more importantly, at what cost.

The good news is that you have complete control over it. Pay on time, keep your utilisation low, avoid unnecessary enquiries, and check your report regularly. With the new 2026 RBI rules making your score update faster than ever, your good habits will also be rewarded faster than before.

The rule is simple: treat every EMI and every credit card bill as non-negotiable. Do that consistently, and your CIBIL score will take care of itself.

Read Next on Simplix

- What Is a Credit Card? A Complete Beginner’s Guide for India

- The Minimum Due Trap — Why Paying Less Is Costing You More [link]

- Explore All CIBIL Score & Credit Health Guides

Want to check your CIBIL score right now?

You are entitled to one free credit report every quarter under RBI rules. Check yours today on the official CIBIL website — it takes less than 2 minutes and does not affect your score.

👉 Check Your Free CIBIL Score → CIBIL Website

Looking for a credit card that helps you build your score? Explore Simplix’s curated picks for the best beginner-friendly credit cards in India.

👉 Best Credit Cards for Beginners in India → [Add affiliate link here]