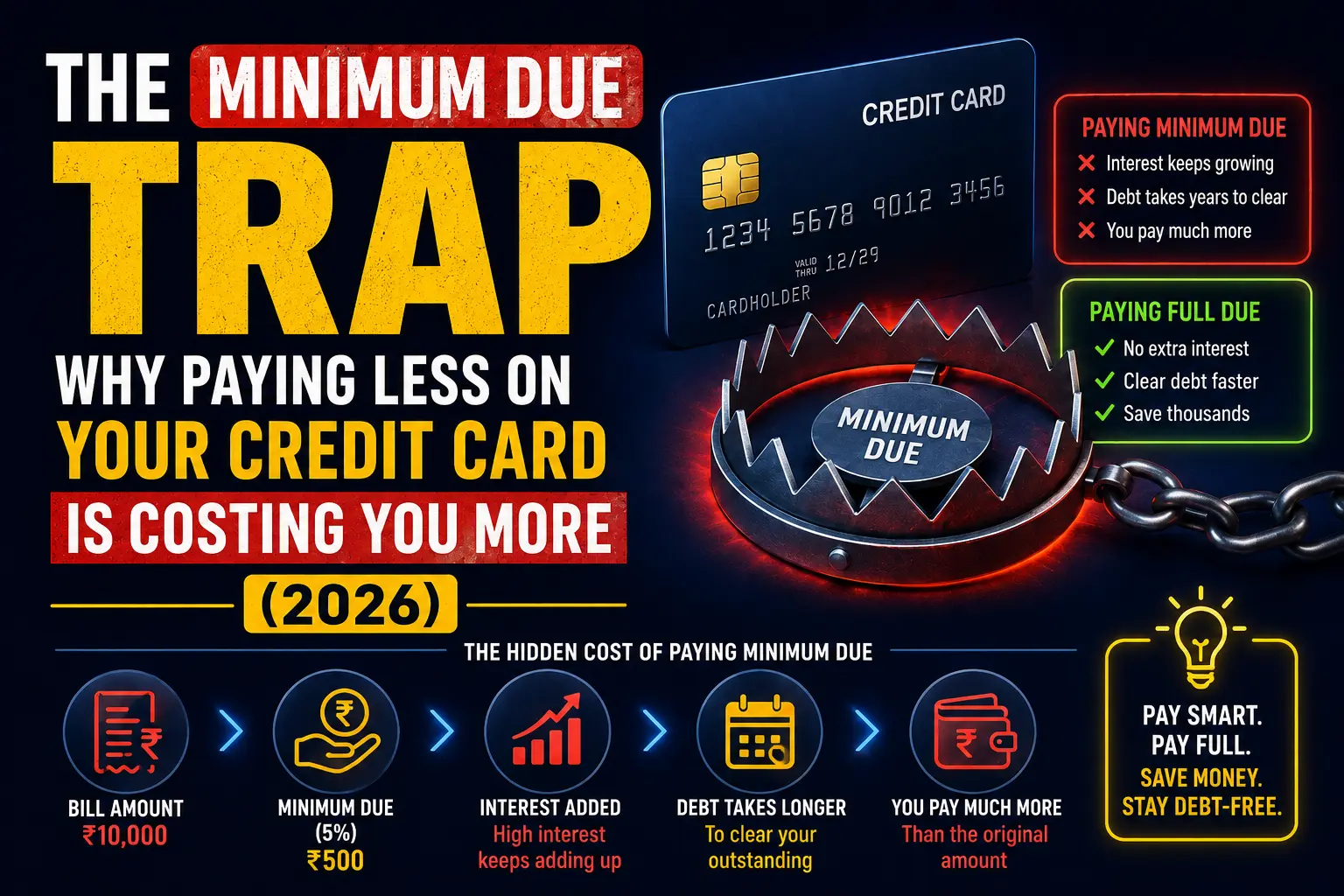

Every month, your credit card statement shows two numbers — the Total Amount Due and the Minimum Amount Due. 😬 Millions of Indians choose the smaller number, pay it, and move on — convinced they have handled their bill responsibly.

Surprisingly, that one decision quietly costs them thousands of rupees every single year. Moreover, most of them never realise it until the debt has already grown well beyond control.

In this guide, we explain exactly how the minimum due trap works, how banks calculate it, what it actually costs you with real numbers, and — most importantly — how to break free from it for good.

Table of Contents

- What Is the Minimum Due on a Credit Card?

- How Banks Calculate the Minimum Due

- The Real Cost — A Real Indian Example

- The Grace Period Trap Nobody Talks About

- How the Minimum Due Affects Your CIBIL Score

- What the RBI Now Mandates About Minimum Due

- The Debt Spiral — How It Happens Step by Step

- How to Break Free from the Minimum Due Trap

- When Is It Okay to Pay Only the Minimum Due?

- Final Verdict

1. What Is the Minimum Due on a Credit Card?

The minimum due refers to the smallest amount your bank asks you to pay each month to avoid a late payment fee and keep your account in good standing. Typically, banks set this at around 5% of your total outstanding balance — although the exact formula varies across banks.

On the surface, it sounds like a helpful feature — a safety net for months when money feels tight. However, in reality, it functions more like a carefully designed mechanism that keeps you owing the bank money for as long as possible while collecting maximum interest along the way.

“Minimum Amount Due sounds like safety. It means you will not get a late payment mark. It does not mean the bank stops charging you interest on the rest.” — Simplix Finance Desk

2. How Banks Calculate the Minimum Due

There is no single RBI-mandated formula for calculating the minimum due. Consequently, each bank follows its own method. However, the RBI does mandate that the minimum due must cover the full interest amount plus a portion of the principal — so that your debt does not keep growing even as you pay.

In practice, most major Indian banks calculate it as follows:

Minimum Due Formula:

Higher of (100% of all interest + fees + taxes) OR (5% of total outstanding) + any past-due amounts + EMI instalments due that month + overlimit charges

For example, suppose your HDFC Bank statement shows a total outstanding of ₹60,000. Furthermore, assume your monthly interest rate runs at 3.5% and the bank has charged ₹500 in fees. In that scenario:

| Component | Amount |

|---|---|

| 5% of ₹60,000 outstanding | ₹3,000 |

| Interest for the month (3.5% of ₹60,000) | ₹2,100 |

| Fees and GST | ₹500 |

| Minimum Due (higher of the above + fees) | ≈ ₹3,500 |

Notice that the minimum due of ₹3,500 barely covers the interest and fees. As a result, you pay ₹3,500 and your outstanding balance drops by only a few hundred rupees — while the remaining ₹56,500+ continues attracting interest next month.

3. The Real Cost — A Real Indian Example

Let us make this concrete with numbers. Suppose you spend ₹50,000 on your credit card — perhaps for a new phone, a flight booking, and monthly groceries combined. Your bank charges an interest rate of 36% per year (3% per month) — a rate common across many Indian credit cards.

Scenario A — You Pay Only the Minimum Due (5%) Each Month

Your minimum due for month one comes to approximately ₹2,500. You pay it and feel relieved. However, the remaining ₹47,500 now attracts 3% monthly interest — adding ₹1,425 in interest alone to your next month’s balance.

Furthermore, each month your minimum due shrinks slightly as your balance reduces — but so does the principal repayment. In total, paying only 5% minimum due on ₹50,000 at 36% annual interest means:

| What You Owe | Minimum Due Only | Full Payment |

|---|---|---|

| Starting Balance | ₹50,000 | ₹50,000 |

| Total Interest Paid | ₹30,000+ | ₹0 |

| Time to Clear Debt | 3–4 years | Next billing cycle |

| Total Amount Paid | ₹80,000+ | ₹50,000 |

That ₹50,000 purchase effectively costs you over ₹80,000 — just because you chose the smaller number on your statement every month. Additionally, the RBI now requires banks to print exactly this calculation on your statement — showing you how long full repayment takes on minimum payments alone. Check your next statement. That number will surprise you.

4. The Grace Period Trap Nobody Talks About

Here is the part of the minimum due trap that most people never discover until it hits them. When you pay only the minimum due — even if you pay it on time — your bank immediately cancels your grace period for the next billing cycle.

Normally, your credit card gives you 18 to 21 interest-free days after your statement date. However, the moment you carry any unpaid balance forward, the bank starts charging interest on your new purchases from the very day you make them — not from your next statement date.

In other words, the interest-free window completely disappears. Consequently, even the grocery run you do the next day after paying your minimum due starts accumulating interest from that day itself — not at the end of the billing cycle.

The grace period only works when you clear your full outstanding balance every month. Carry even ₹1 forward, and the bank starts the interest clock on every new transaction immediately. — Simplix Finance Desk

5. How the Minimum Due Affects Your CIBIL Score

Many cardholders believe that paying the minimum due on time keeps their CIBIL score safe. Technically, that belief holds some truth — paying the minimum due on time does prevent a late payment mark on your report. However, the full picture looks significantly more complicated.

High Credit Utilisation Hurts Your Score

When you pay only the minimum due month after month, your outstanding balance stays high relative to your credit limit. For instance, if your limit stands at ₹1,00,000 and your balance consistently stays above ₹60,000, your credit utilisation hits 60% — well above the recommended 30% threshold. As a result, your CIBIL score drops even though you never miss a payment.

Banks Flag Minimum Due Payers Internally

Moreover, banks maintain internal risk profiles separate from CIBIL. Consistently paying only the minimum due flags you internally as a high-risk revolver — someone who carries debt rather than repays it. This internal flag can affect your eligibility for credit limit increases, balance transfer offers, and even future loan approvals from the same bank.

Fortnightly Reporting Makes It Faster

From 2026, banks report credit card data to bureaus every 15 days under the new RBI mandate. Therefore, a persistently high balance now appears on your CIBIL report much faster than before — compounding the utilisation damage even further.

6. What the RBI Now Mandates About Minimum Due

The RBI has introduced several important protections for cardholders around minimum due payments. Understanding these rules helps you exercise your rights and avoid unfair bank practices.

- Full interest must be covered: The RBI mandates that the minimum due must always cover 100% of the interest, fees, and taxes due — so that your debt does not grow even when you pay the minimum. Banks can no longer set a minimum due so low that your outstanding balance actually increases month over month.

- No compounding of unpaid fees and taxes: The RBI explicitly prohibits banks from adding unpaid levies, taxes, or fees to your principal for interest calculation purposes. In other words, the bank cannot charge you interest on your late payment fee — only on the actual outstanding principal.

- Repayment timeline warning mandatory: Every credit card statement must now include a clear warning showing exactly how many months it will take to clear your balance if you keep paying only the minimum due. This disclosure requirement directly addresses the opacity that kept millions of Indians trapped in revolving debt.

- Interest only on unpaid portion: Following a Supreme Court directive, banks cannot charge interest on the portion of your bill you have already paid. Previously, many banks charged interest on the entire billed amount even if you paid 90% of it. That practice is now prohibited.

7. The Debt Spiral — How It Happens Step by Step

Understanding the debt spiral helps you recognise it before it starts. Here is exactly how a well-intentioned cardholder ends up trapped in months of revolving debt.

Month 1: You spend ₹40,000 on your card. The statement arrives. You see ₹2,000 as the minimum due and pay it — feeling financially responsible.

Month 2: Your bank charges 3% monthly interest on the unpaid ₹38,000 — adding ₹1,140 to your balance. You also spend ₹15,000 more this month. Additionally, since you did not pay in full last month, the bank charges interest on the new ₹15,000 from day one — not from the statement date. Your new total: ₹54,140+.

Month 3: Your balance has grown despite your payments. Furthermore, the minimum due has also grown — now requiring ₹2,700. You pay it, but your outstanding continues to creep upward. The cycle tightens.

Month 6 onwards: You now carry a balance that exceeds your original spend. Your CIBIL score starts reflecting high utilisation. Your bank flags your account internally as a revolver. The trap has fully closed.

8. How to Break Free from the Minimum Due Trap

Fortunately, escaping the minimum due trap follows a clear and practical path. Moreover, the earlier you start, the faster you recover.

Step 1 — Stop Adding New Purchases to the Card

First, stop using the card for new spending until you clear the outstanding balance. Every new purchase on a card with an unpaid balance attracts interest from day one — accelerating the spiral further.

Step 2 — Pay More Than the Minimum Every Month

Even paying double the minimum due significantly reduces your interest burden and shortens your repayment timeline. Therefore, treat the minimum due as the absolute floor — not the target.

Step 3 — Consider a Balance Transfer

Many Indian banks offer balance transfer facilities that move your outstanding balance to a new card at a lower interest rate — sometimes as low as 0% for an introductory period of 3 to 6 months. Consequently, a well-timed balance transfer can save thousands in interest while you focus on clearing the principal.

Step 4 — Convert to an EMI

Most banks allow you to convert your outstanding credit card balance into a structured EMI plan at a significantly lower interest rate than the standard revolving rate. For instance, an outstanding balance attracting 36% annual interest on revolving credit might convert to an EMI plan at 14–18% annually — cutting your interest cost nearly in half.

Step 5 — Set Up Autopay for the Full Amount Going Forward

Once you clear your outstanding balance, set up autopay immediately for the full outstanding amount — not the minimum due. This single habit permanently protects you from ever falling into the minimum due trap again.

9. When Is It Okay to Pay Only the Minimum Due?

Almost never. However, there exists one narrow exception where it makes reasonable sense:

If you face a genuine one-month cash flow crunch — your salary delays, an emergency arises, or a large planned expense depletes your account — paying the minimum due for one single month costs you approximately 3 to 3.5% in interest on the outstanding balance. That is an acceptable short-term cost if you commit to clearing the full balance the following month without exception.

Beyond that single exception, there is no scenario where consistently paying only the minimum due serves your financial interests. The interest you pay always exceeds the rewards, cashback, or convenience the card provides.

10. Final Verdict

The minimum due trap works precisely because it feels responsible. You paid your bill. You avoided a late payment fee. Your account shows no overdue amount. However, none of that changes the fact that the bank charges you 24% to 48% annual interest on everything you did not pay — starting immediately.

The rule at Simplix is simple and non-negotiable: always pay your full outstanding balance before the due date. Not the minimum. Not a round number. The full amount.

Moreover, set up autopay for the total amount due today — not the minimum due option. That one action eliminates the risk of ever accidentally paying less than you should. Your CIBIL score, your wallet, and your future self will thank you for it.

Read Next on Simplix

- How Credit Card Billing Cycles Work — And How to Use Them to Your Advantage

- What Is a CIBIL Score? How It Works and Why It Matters

- Secured vs Unsecured Credit Cards — Which One Should You Get First?

Carrying a credit card balance you want to clear faster?

Explore Simplix’s curated picks for the best balance transfer credit cards and low-interest cards in India — compared and simplified so you make the right move.

👉 Explore Best Lifetime Free Credit Cards in India

Get one clear, practical finance tip every week — no spam, no filler. Follow Simplix on Instagram.

👉 Follow Simplix on Instagram → Simplix MultiVentures