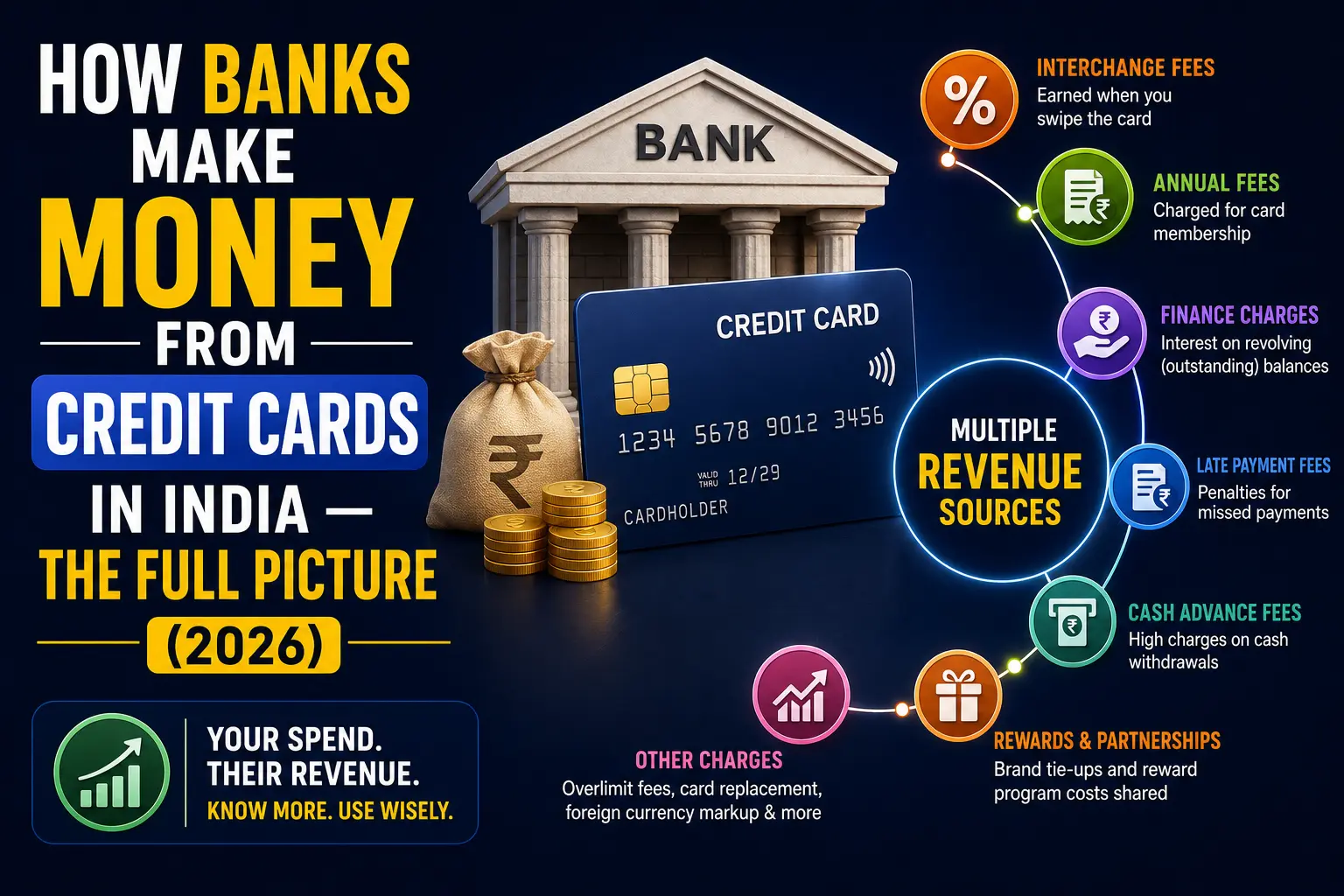

Every time you swipe your credit card, someone makes money. 💰 And surprisingly, that someone is not always just the bank that issued your card — it is an entire ecosystem of financial players collecting their share of every single transaction you make.

Furthermore, banks make money from your credit card even when you pay your bills in full and on time, never pay a single rupee in interest, and avoid every fee on your statement. That fact alone surprises most cardholders — and understanding it completely changes how you think about the rewards, cashback, and perks your card offers you.

In this guide, we break down every revenue stream banks use to profit from credit cards in India — so you understand exactly what powers the system you participate in every day.

Table of Contents

- The Big Picture — How Banks Earn From Cards

- Revenue Stream 1 — Interest Charges

- Revenue Stream 2 — Interchange Fees

- Revenue Stream 3 — Cardholder Fees

- Revenue Stream 4 — Cash Advance Fees

- Revenue Stream 5 — Co-Branded & Partnership Revenue

- Revenue Stream 6 — EMI Conversion & Balance Transfer Fees

- Why Banks Offer Rewards and Cashback

- How This Knowledge Helps You as a Cardholder

- Final Verdict

1. The Big Picture — How Banks Earn From Cards

Indian credit card issuers draw revenue from two broad groups: cardholders and merchants. Cardholders pay through interest charges and various fees. Merchants pay through interchange fees on every transaction. Together, these two streams fund the entire credit card ecosystem — including the rewards and cashback programmes that banks offer to attract new customers.

According to data from the Indian Banking and Economics Finance Institute, interest income contributes 40 to 50% of total credit card revenue for Indian banks. Interchange fees add another 20 to 25%. The remaining 25 to 35% comes from cardholder fees, partnership income, and other charges.

“A credit card is not a charity. Every benefit your bank offers you — cashback, reward points, lounge access — has a funding mechanism behind it. Understanding that mechanism makes you a smarter cardholder.” — Simplix Finance Desk

2. Revenue Stream 1 — Interest Charges

Interest charges represent the single largest revenue source for credit card issuers in India. Banks charge interest on any outstanding balance a cardholder carries beyond the due date — at annual rates that typically range between 18% and 42% per annum depending on the bank and card type.

In India, most credit card issuers apply a monthly interest rate of 2% to 3.5% on unpaid balances — which translates to an effective annual rate of 24% to 42%. Consequently, a cardholder who carries a ₹50,000 balance for 12 months pays anywhere between ₹12,000 and ₹21,000 in interest alone — on top of the original amount.

The Minimum Due Connection

This revenue stream connects directly to the minimum due trap we covered in our previous Simplix guide. Banks deliberately structure the minimum due at a low 5% of outstanding balance — because a cardholder who pays only the minimum continues generating interest income for the bank month after month. Moreover, the longer that cardholder carries a balance, the more profitable they become for the issuer.

Simplix Insight: A cardholder who pays their bill in full every month generates zero interest revenue for the bank. Therefore, banks design their rewards programmes specifically to attract and retain this group — because they compensate through interchange fees and annual fees instead.

3. Revenue Stream 2 — Interchange Fees

Interchange fees represent the most misunderstood revenue stream in the credit card ecosystem. Most cardholders have never heard of them — yet these fees power the cashback and rewards programmes banks offer.

Here is how the interchange fee works: every time a cardholder uses their credit card at a merchant, the merchant’s bank pays a fee to the cardholder’s bank (the issuing bank) for processing that transaction. In India, banks typically charge between 1.2% and 2% as the interchange fee across different card and customer segments — and this contributes approximately 20 to 25% of total credit card revenue for Indian issuers.

A Real Example

Suppose you spend ₹10,000 at a restaurant using your HDFC Bank credit card. The restaurant’s bank pays HDFC approximately ₹150 to ₹200 as the interchange fee. HDFC then uses a portion of that — perhaps ₹50 to ₹75 — to fund the reward points or cashback it credits to your account. The rest stays as pure revenue for the bank.

In other words, merchants effectively subsidise your rewards — a fact that most cardholders never realise. Furthermore, this also explains why merchants who accept card payments price their goods slightly higher than those who operate cash-only.

| Party | Role | What They Earn / Pay |

|---|---|---|

| Cardholder | Makes the purchase | Earns rewards funded by interchange |

| Issuing Bank (e.g. HDFC) | Issues the card | Receives 1.2–2% interchange fee |

| Card Network (Visa/Mastercard/RuPay) | Processes the transaction | Earns a small assessment fee (~0.1%) |

| Merchant’s Bank | Collects payment for merchant | Pays interchange, earns MDR spread |

| Merchant | Sells the product or service | Receives payment minus total MDR fees |

4. Revenue Stream 3 — Cardholder Fees

Beyond interest, banks collect a range of fees directly from cardholders. These fees form a predictable, recurring revenue layer that banks earn regardless of whether a cardholder pays interest or not.

Annual / Joining Fees

Many credit cards charge a joining fee at the time of issuance and an annual renewal fee each year thereafter. Premium cards like the HDFC Diners Club Black charge ₹10,000 or more annually — while entry-level cards charge ₹500 to ₹1,000. However, most banks waive these fees if cardholders meet a minimum annual spend threshold.

Late Payment Fees

Banks charge late payment fees when cardholders miss their due date. In India, these fees typically range from ₹100 to ₹1,300 depending on the outstanding balance — and the RBI caps the maximum amount banks can charge based on the outstanding balance slab.

Over-Limit Fees

When a cardholder spends beyond their sanctioned credit limit, the bank charges an over-limit fee — typically 2.5% of the amount exceeding the limit. Additionally, this triggers a hard flag on the cardholder’s credit report, potentially hurting their CIBIL score.

Foreign Transaction Fees

Most Indian credit cards charge a foreign currency markup of 1.5% to 3.5% on international transactions — in addition to the exchange rate applied. On a ₹1,00,000 international purchase, that markup alone costs the cardholder ₹1,500 to ₹3,500 in additional charges.

5. Revenue Stream 4 — Cash Advance Fees

Banks allow cardholders to withdraw cash using their credit cards — but this feature carries one of the heaviest cost structures in the entire banking ecosystem. Consequently, banks earn significantly from cardholders who use this facility.

When a cardholder withdraws cash using a credit card, the bank charges:

- A cash advance fee — typically 2.5% to 3% of the amount withdrawn, subject to a minimum of ₹250 to ₹500

- Interest from day one — unlike regular purchases, cash advances carry no grace period. The bank starts charging interest from the moment of withdrawal, not from the statement date

- Higher interest rates — some banks charge a higher monthly rate on cash advances than on regular purchases

In other words, a ₹20,000 cash withdrawal on a credit card costs the cardholder ₹500 to ₹600 in upfront fees plus interest at 36 to 42% annually from day one. Therefore, Simplix strongly advises against using a credit card for cash withdrawals under any circumstances except a genuine emergency.

6. Revenue Stream 5 — Co-Branded & Partnership Revenue

Co-branded credit cards represent a growing and highly profitable revenue stream for Indian banks. A co-branded card carries the brand of both the bank and a partner company — such as the Amazon Pay ICICI Card, the Air India SBI Card, or the Flipkart Axis Bank Card.

In these arrangements, the partner brand pays the bank to issue and promote the card, often covering a portion of the reward costs in exchange for customer loyalty and increased spend on their platform. Moreover, the bank earns higher interchange fees on co-branded cards because these cards drive higher transaction volumes among loyal brand customers.

Additionally, banks earn revenue from data partnerships — using aggregated, anonymised spending data to understand consumer behaviour and offer targeted financial products. This data becomes increasingly valuable as card usage grows across India.

7. Revenue Stream 6 — EMI Conversion & Balance Transfer Fees

Banks earn additional revenue when cardholders convert large purchases into EMIs or transfer balances from other cards. Specifically:

EMI Conversion Fees

When a cardholder converts a purchase into a credit card EMI, the bank charges a processing fee of 1% to 3% of the transaction amount — in addition to the interest rate on the EMI plan, which typically runs between 14% and 18% annually. Furthermore, many banks also charge a foreclosure fee of 2 to 3% if the cardholder wants to close the EMI plan before the tenure ends.

Balance Transfer Fees

Balance transfer facilities — where a cardholder moves outstanding debt from one card to another at a lower introductory rate — carry a transfer fee of 1% to 2% of the amount transferred. While these facilities genuinely help cardholders reduce interest costs, banks still earn a processing fee upfront plus interest after the introductory period ends.

8. Why Banks Offer Rewards and Cashback

Understanding bank revenue streams makes the logic behind rewards programmes immediately clear. Banks offer cashback, reward points, and lounge access for two specific reasons:

First, rewards drive spending volume. The more a cardholder spends, the more interchange fee revenue the bank earns. A cardholder who routes all their monthly expenses through a single card generates significantly more interchange revenue than someone who uses the card occasionally. Rewards programmes incentivise that behaviour directly.

Second, rewards attract and retain profitable customers. A cardholder who spends heavily and pays in full every month generates consistent interchange revenue with zero interest cost to manage. Banks compete intensely for this customer segment — which is why premium cards offer premium rewards.

In practice, banks typically return 25 to 35% of interchange revenue to cardholders through rewards. The remainder stays as profit. Moreover, a significant portion of reward points and cashback earned never actually redeems — either because cardholders forget, let points expire, or find redemption processes too complicated. This unredeemed value adds directly to bank revenue.

Simplix Insight: The best credit card strategy uses this knowledge to your advantage — spend enough to earn meaningful rewards, always pay in full to avoid interest, and redeem every point before expiry. That way, the bank funds your rewards through merchant interchange fees rather than your interest payments.

9. How This Knowledge Helps You as a Cardholder

Understanding how banks profit from credit cards gives you a clear framework for using your card in a way that maximises your benefit and minimises theirs. Specifically:

- Always pay in full — eliminate interest revenue entirely. The bank earns only interchange fees from you, which it partially returns as rewards anyway

- Avoid cash advances — the fee structure and immediate interest make this one of the most expensive banking services available to Indian consumers

- Redeem rewards before expiry — unredeemed points and cashback go back to the bank. Track your rewards and redeem them actively

- Check foreign markup fees — if you travel internationally, choose a card with zero or low forex markup. The difference on a ₹1,00,000 spend can exceed ₹3,000

- Understand co-branded cards — these cards work best if you genuinely use the partner brand regularly. Otherwise, a general rewards card delivers better value

- Time EMI conversions carefully — only convert to EMI when the interest rate falls below what a personal loan would cost you. Otherwise, a personal loan may offer better terms

10. Final Verdict

Banks design credit cards as profit-generating tools — not consumer benefits programmes. However, understanding the revenue model behind your card gives you something most cardholders never have: the ability to use the system deliberately, rather than reactively.

When you pay in full every month, avoid unnecessary fees, and redeem every reward you earn, you shift the equation in your favour. The bank still earns its interchange fee from merchants — but you keep the rewards, pay zero interest, and build your CIBIL score at the same time.

In other words, the best credit card user is the one the bank designed the product to attract — but the one who costs them the least while taking the most value. Aim to be that cardholder.

Read Next on Simplix

- The Minimum Due Trap — Why Paying Less Is Costing You More

- What Is a CIBIL Score? How It Works and Why It Matters

- Secured vs Unsecured Credit Cards — Which One Should You Get First?

Want to pick a card that works for you — not just the bank?

Simplix has curated the best credit cards in India by rewards, fees, and actual value — so you earn more and pay less.

👉 Explore Best Lifetime Credit Cards in India

Get one practical finance insight every week — no spam, just clarity.

👉 Follow Simplix on Instagram → Simplix MultiVentures