When most people think about credit cards, they picture the standard kind — apply online, get approved or rejected, and receive the card. However, that describes only one of two fundamentally different types of credit cards India offers. 💳 And the one you choose first can shape your financial journey for years ahead. One totally missing topic here is secured credit cards.

Surprisingly, around 48% of all fresh credit card applications in India get rejected at the underwriting stage — most commonly due to a low CIBIL score or insufficient income proof. Furthermore, many of those applicants had no idea a better-suited option already existed for their situation.

In this guide, we break down exactly what secured and unsecured credit cards are, how they differ, who qualifies for each, and which one makes more sense for your situation right now.

Table of Contents

- What Is a Secured Credit Card?

- What Is an Unsecured Credit Card?

- Secured vs Unsecured — Full Comparison

- Who Should Get a Secured Credit Card?

- Who Should Get an Unsecured Credit Card?

- Best Secured Credit Cards in India (2026)

- Best Unsecured Beginner Cards in India (2026)

- How a Secured Card Builds Your CIBIL Score

- When to Upgrade from Secured to Unsecured

- Final Verdict

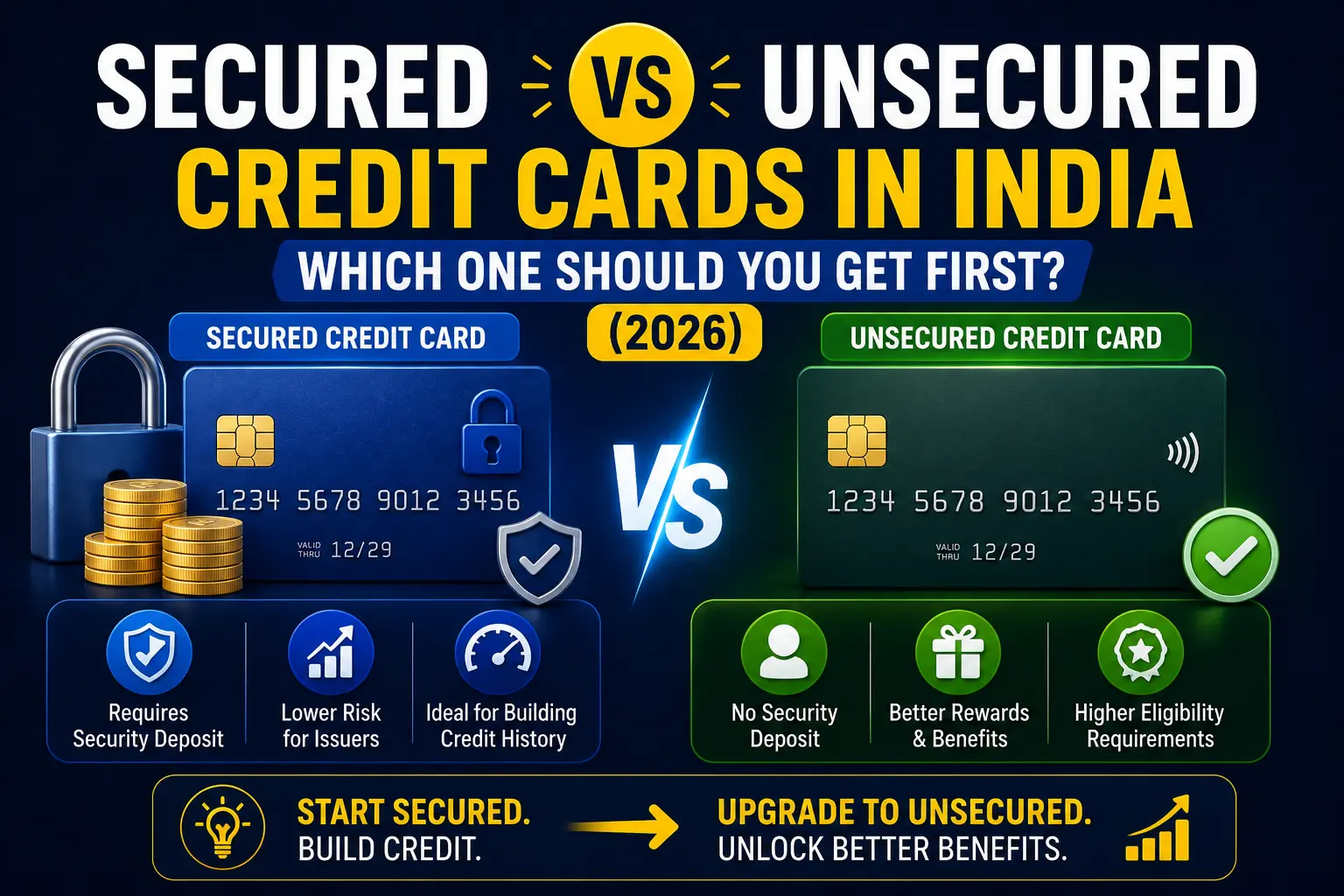

1. What Is a Secured Credit Card?

A secured credit card requires you to place a fixed deposit (FD) with the bank as collateral before the bank issues the card. The bank then sets your credit limit at 70% to 90% of the FD value. So if you place an FD of ₹50,000, your credit limit typically falls between ₹35,000 and ₹45,000.

Importantly, your FD continues to earn interest throughout the entire period — the bank does not freeze or consume it unless you default on your payments. In other words, your money keeps growing in the background while you use the card for everyday spending.

Moreover, secured cards carry no minimum income requirement and no CIBIL score threshold. Banks approve the card purely on the basis of the FD you place — making them accessible to students, homemakers, freelancers, and anyone building their credit profile from scratch.

“A secured credit card lets you use borrowed money while your own money earns interest in the background. Used wisely, it builds your credit history without putting your finances at risk.” — Simplix Finance Desk

2. What Is an Unsecured Credit Card?

An unsecured credit card requires no collateral, no FD, and no security deposit. Instead, banks approve applications based entirely on your credit profile, income stability, and repayment history. The bank takes on the full risk — which is why eligibility requirements are significantly stricter.

Most Indian banks require a minimum CIBIL score of 700 or above for unsecured card applications. However, some issuers like SBI Cards and Bajaj Finserv go as low as 650 for specific entry-level products. Additionally, most banks require a minimum monthly income of ₹15,000 to ₹25,000 for salaried applicants — and self-employed applicants must submit ITR documents for the last two years.

Unsecured cards typically offer better rewards, higher credit limits, and more premium features than secured cards. Consequently, they suit individuals who already have an established credit history and a stable income.

3. Secured vs Unsecured — Full Comparison

Here is a clear side-by-side breakdown of how both card types differ across every key factor:

| Factor | Secured Card | Unsecured Card |

|---|---|---|

| Collateral | Fixed Deposit required | No collateral needed |

| CIBIL Score | None — no minimum | 700+ (some accept 650) |

| Income Proof | Not required | Mandatory |

| Credit Limit | 70–90% of FD value | Based on income & profile |

| FD Earns Interest | Yes — continues earning | Not applicable |

| Approval Rate | Very high with FD | ~52% industry-wide |

| Rewards & Perks | Basic to moderate | Better rewards, travel perks |

| Best For | No history, low CIBIL, no income proof | Salaried / self-employed with credit history |

| Upgrade Path | Convert to unsecured after 12–18 months | Already unsecured |

4. Who Should Get a Secured Credit Card?

You Have No Credit History

If your CIBIL report shows -1 or NH (No History), banks cannot evaluate your creditworthiness — and most reject an unsecured card application outright. A secured card solves this problem immediately. You place an FD, get the card, use it for small purchases, pay in full every month, and within 6 to 12 months your CIBIL score builds to a level that qualifies you for unsecured cards.

Your CIBIL Score Falls Below 700

Therefore, if your score currently sits between 550 and 699 — perhaps due to a past missed payment or a settled loan — a secured card gives you an active way to rebuild your score rather than simply waiting for time to heal old marks on its own.

You Have No Income Proof

Students, homemakers, freelancers, and early-stage self-employed individuals often struggle to produce the formal income documentation banks require for unsecured cards. Secured cards eliminate this barrier entirely. You need only the FD amount — no salary slips, no ITR, no employer verification.

You Want a Low-Risk Way to Start

Additionally, a secured card works well for anyone who wants to learn responsible credit habits without the risk of accumulating unmanageable debt. Since your credit limit ties directly to your FD, overspending beyond your means becomes structurally harder.

5. Who Should Get an Unsecured Credit Card?

An unsecured credit card suits individuals who already have the financial foundation in place. Specifically, go straight for an unsecured card if:

- Your CIBIL score stands at 700 or above

- You earn a stable monthly income of ₹15,000 or more as a salaried employee

- You have at least 6 months of credit history — a previous loan, add-on card, or any credit product

- You want access to better rewards, cashback, airport lounge access, or travel perks

- You prefer not to lock capital in an FD to access credit

Moreover, if your employer credits your salary into an account with a major bank like HDFC, ICICI, or Axis, that bank may offer you a pre-approved credit card based on your salary history alone — often without a hard CIBIL enquiry. Check your bank’s app or net banking portal before applying anywhere else.

6. Best Secured Credit Cards in India (2026)

| Card | Min FD | Credit Limit | Key Benefit |

|---|---|---|---|

| SBI Unnati Card | ₹25,000 | Up to 90% of FD | No annual fee for first 4 years |

| Kotak 811 #DreamDifferent | ₹10,000 | Up to 90% of FD | Lifetime free, app-based approval |

| HDFC MoneyBack (Secured) | ₹25,000 | Up to 80% of FD | Cashback on online spends |

| ICICI Bank Instant Platinum | ₹20,000 | Up to 85% of FD | EMI facility, fuel surcharge waiver |

| Axis Bank Insta Easy | ₹10,000 | Up to 80% of FD | Instant approval, lifetime free |

Simplix Pick: For the lowest FD minimum and a lifetime free card, the Kotak 811 #DreamDifferent at ₹10,000 FD is the easiest starting point. Additionally, the Axis Bank Insta Easy offers instant approval entirely through the app — no branch visit needed.

7. Best Unsecured Beginner Cards in India (2026)

| Card | Annual Fee | Min CIBIL | Best For |

|---|---|---|---|

| Amazon Pay ICICI Card | Lifetime Free | 700+ | Amazon shoppers — 5% cashback on Prime |

| Axis Bank Ace Card | ₹499 (waivable) | 700+ | Utilities — 5% cashback via Google Pay |

| IDFC First Select Card | Lifetime Free | 700+ | Reward points, zero forex markup |

| SBI SimplyCLICK Card | ₹499 (waivable) | 650+ | Online shopping — 10x points on Amazon |

| HDFC MoneyBack+ Card | ₹500 (waivable) | 700+ | Cashback on online and offline spends |

Simplix Pick: For your first unsecured card, prioritise lifetime free options like the Amazon Pay ICICI Card or IDFC First Select Card. No annual fee means no pressure to hit a minimum spend — and keeping them open long-term helps your credit age factor.

8. How a Secured Card Builds Your CIBIL Score

Many first-time applicants worry that a secured card does not build credit the same way an unsecured card does. Fortunately, that concern is unfounded. Banks report secured card payment behaviour to credit bureaus exactly the same way they report unsecured card data — your CIBIL score cannot distinguish between the two.

Therefore, every on-time payment on your secured card adds a positive entry to your credit history. Furthermore, keeping your utilisation below 30% of your FD-linked limit builds your score faster by demonstrating disciplined spending behaviour.

In practice, most cardholders who use a secured card responsibly — paying in full every month and keeping utilisation low — build their CIBIL score from zero to 750+ within 12 to 18 months. At that point, the best unsecured cards in the market become available to them.

9. When to Upgrade from Secured to Unsecured

Path 1 — Direct Upgrade with the Same Bank

Most banks that issue secured cards offer a direct upgrade path once you meet their threshold. Typically, the bank reviews your account after 12 to 18 months of consistent on-time payments and either converts your card automatically or invites you to apply for an unsecured variant. At that point, the bank also releases your FD back to you in full.

Path 2 — Apply Fresh with a Different Bank

Alternatively, once your CIBIL score crosses 700 through secured card usage, you can apply for a new unsecured card with any bank — not just the one that issued your secured card. This path gives you more choice and lets you pick the card with the best rewards for your actual spending habits.

However, avoid closing your secured card immediately after getting the unsecured one. Instead, keep it open with minimal usage — the credit age and available limit it contributes continue to benefit your CIBIL score.

10. Final Verdict

The secured vs unsecured question does not have a universal answer. Rather, it depends entirely on where you currently stand in your credit journey.

If you have no credit history, a low CIBIL score, or no income proof — start with a secured credit card. Place an FD of ₹10,000 to ₹25,000, use the card for small monthly purchases, pay in full every month, and let your CIBIL score build itself over 12 to 18 months. The upgrade path to an unsecured card is clear, proven, and well-supported by every major Indian bank.

If you already have a CIBIL score of 700 or above and stable income proof — go directly for a lifetime free unsecured card that matches your spending habits. Start with one card, use it responsibly, and add more only after your first card’s credit history matures.

Either way, the goal remains the same: build a strong credit foundation that opens every financial door you will need in the future — home loans, car loans, business credit, and the best interest rates the market offers.

Read Next on Simplix

- What Is a Credit Card? A Complete Beginner’s Guide for India

- What Is a CIBIL Score? How It Works and Why It Matters

- The Minimum Due Trap — Why Paying Less Is Costing You More

Not sure which card suits your situation right now?

Simplix has curated the best secured and unsecured credit cards in India — compared by FD minimum, rewards, eligibility, and upgrade path.

👉 Explore Best Lifetime Free Credit Cards in India

Follow Simplix on Instagram for weekly finance guides — no spam, just clarity.

👉 Follow Simplix on Instagram → Simplix MultiVentures